China's scenic installation capacity in 2021 will be similar to that of the European market and the U.S. market combined, and in the InfoLink launch of the 2021-2030 Global Wind Energy Storage White PaperIn other words, China is not only the largest market for renewable energy, but also the fastest growing market in the next ten years. The following excerpts from the white paper illustrate how China has maintained its growth during the high base period. The following excerpts from the white paper illustrate how China has maintained its growth momentum from a high base.

China's PV and onshore wind markets are in very similar conditions, with oversupply in the supply chain allowing developers to enjoy low construction costs, and flat prices being the main reason why wind has been able to maintain its growth momentum, and we estimate that the current LCOE for both is between 28-30 USD/MWh. China is one of the world's cheapest photovoltaic prices, manufacturers to pursue the scale and competition caused by the expansion of the wave, resulting in China has the world's most complete photovoltaic supply chain, but also so that China's developers can enjoy the low cost of construction; onshore wind power is also a long time in the over-competition, wind turbines and towers accounted for the onshore wind farms Capital Expenditures (CapEx) of nearly eighty percent, and per kilowatt wind turbine offer in the rush to install the wave after the can fall to 1,500-2,000 yuan (RMB). The price per kilowatt of wind turbine can be reduced to RMB 1,500-2,000 (about US$209.7-279.6) after the rush of installation. Although this is not healthy for the long-term development of the industry, and the price at which manufacturers can maintain a reasonable rate of return should be about RMB 2,500 per kilowatt, it also depresses the cost of construction of wind farms, and maintains the momentum of growth of onshore wind power.

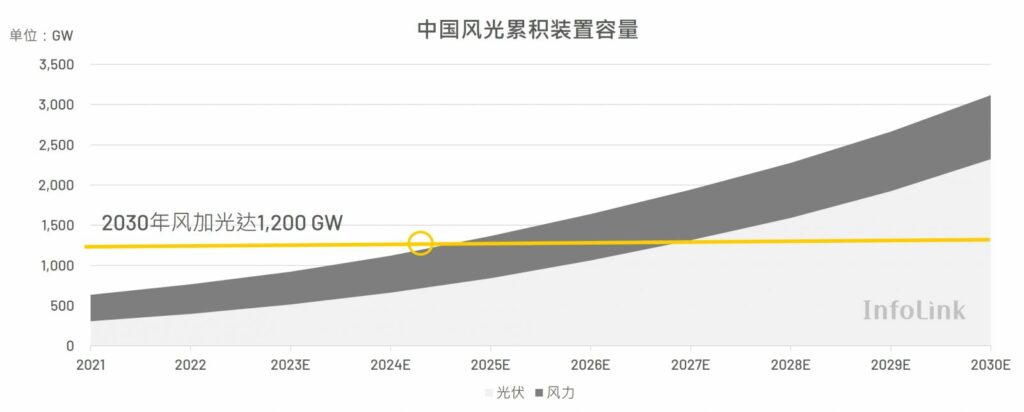

China's renewable energy policy goals are also one of the driving forces for the rapid growth of wind and solar, such as the 14th Five-Year Plan or 2030 wind plus solar installation capacity of 1,200 GW. However, the 2030 target is expected to be reached in the 2025-2026 period, and to reach a single year of 400 GW of new installations in 2030, which means that the growth force generated by manufacturers of spontaneous installation is more powerful than the policy. This means that the growth force generated by the spontaneous installation of manufacturers is stronger than the policy, so we believe that in the growth of photovoltaic, the effect brought about by the flat price is more obvious. Although onshore wind power because of high externalities, the need for field conditions, through the audit are more complicated than the PV, but also can not like PV to distributed, and therefore can not like PV to maintain a high growth rate, but onshore wind power has also reached parity, so in the market spontaneous installation and policy to promote the desert, the Gobi, the desert large-scale wind project to promote the nearly five years will be added to the installation of nearly 200 GW of capacity. And offshore wind power in 2021 after the farewell of wholesale tariffs to enter the phase of parity, although the installation volume has declined, but the total installation volume until 2030 still ranked first among the three major markets, the total installation capacity will come to 82.7GW.

In terms of energy storage, in 2030 China will also replace the United States as the world's largest energy storage market, the device capacity will rise from 10 GWh in 2021 to 415 GWh in 2030, the compound annual growth rate of up to 39 %, and energy storage current construction costs are still high, the need for policy to support the growth of the force, the Chinese government's mandatory norms to make the energy storage market to flourish, the current still Currently, the Chinese government's mandatory regulation has made the energy storage market booming, and the current policy is still dominated by the pre-meter energy storage policy, which requires renewable energy to match with 10-20% and 1-2 hours of energy storage facilities on average, and there are some provinces and sub-provinces proposing policies after the meter, but the business model is still uncertain.

The above is from InfoLink's launch of2021-2030 Global Wind Energy Storage White Paper The following topics are covered in the white paper with more detailed data and reasoning process:

- Wind and solar storage 2021-2030 kWh cost LCOE estimation

- Wind and Solar Storage 2021-2030 Installation Capacity Growth Estimates

- Wind and Solar Storage 2021-2030 Supply Chain Outlook

- Overview and Analysis of the U.S. IRA Act's Wind and Light Storage Related Laws

InfoLink hopes to help enterprises quickly understand the development of the three major global renewable energy markets through this white paper. As a globalized industry, renewable energy is inevitably affected by the policies and supply/demand of the European, U.S., and Chinese markets regardless of which market they are in, and we believe that by utilizing the data in this report, we will be able to ride on the market wave and anticipate the fluctuation of the supply chain price, allocate strategic resources, and identify potential opportunities. strategic resources and identify potential opportunities.

Source: InfoLink

Link to original article:https://www.infolink-group.com/energy-article/cn/wind-topic-the-bright-future-of-chinas-renewable-energy-sector

Special notice: Goodhao is reproduced from other websites for the purpose of transmitting more information rather than for profit, and at the same time does not mean to endorse its views or confirm its description, the content is for reference only. Copyright belongs to the original author, if there is infringement, please contact us to delete.